Category: General Business

How Does GST/HST Apply to Airbnb/Short-term Rentals?

The popularity of Airbnb, short-term rental pools for cottages and vacation properties continues to grow. One aspect of venturing into the short-term rental game is how GST/HST applies. The volume of rental income and the length of the rentals is the determining factor on whether you will need to charge GST/HST.

Essentially, long term-rentals are exempt from GST/HST, while short-term rentals are subject to the tax.

What is considered a short-term rental?

A short-term rental is generally one where the period of occupancy is less than one month and the consideration for the supply is more than $20 a day.

Am I considered a small supplier?

If you are supplying short-term rentals, you will need to determine if you are considered a small supplier for GST/HST purposes. A small supplier is one whose worldwide annual GST/HST taxable supplies, (including zero-rated supplies and including the sales of any associated parties) are less than $30,000, or less than $50,000 for public service bodies (colleges, non-profit organizations, charities, hospitals).

One of the most common oversights we see is forgetting to include any other associated business revenue into the small supplier test.

Should I voluntarily register for GST/HST?

If you are under the $30,000 of taxable supplies for your associated group, you can elect to voluntarily register for GST/HST. The benefits of this would be to enable the claim of any GST/HST paid on expenses related to your short-term rental income. It may also permit you to recover some or all of the GST/HST you may have paid on the unit.

But be aware – if you choose to register, you will be required to collect and remit the GST/HST on your short-term rental income.

There are many factors to consider when venturing into this market; especially if you will be using a portion of your principal residence.

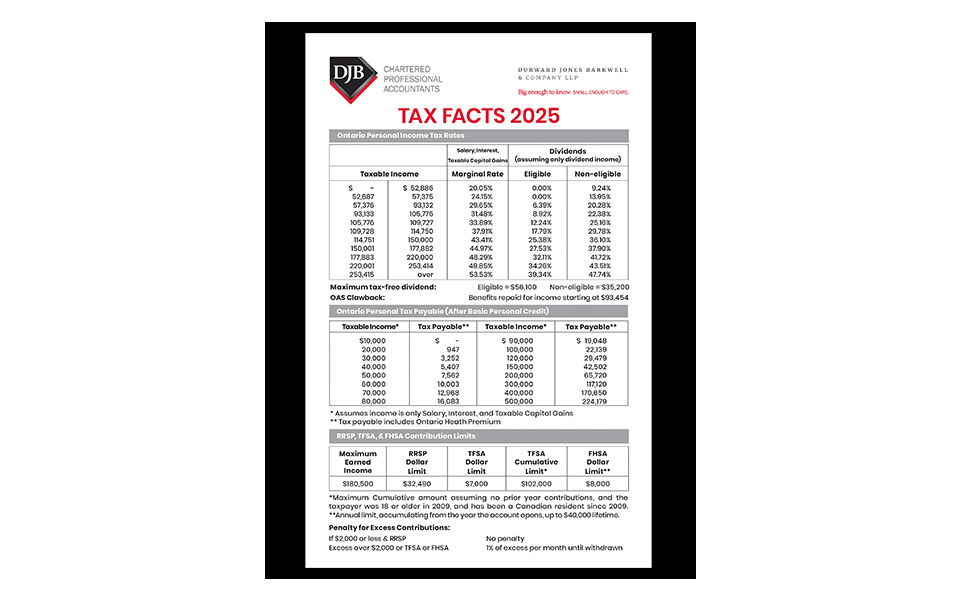

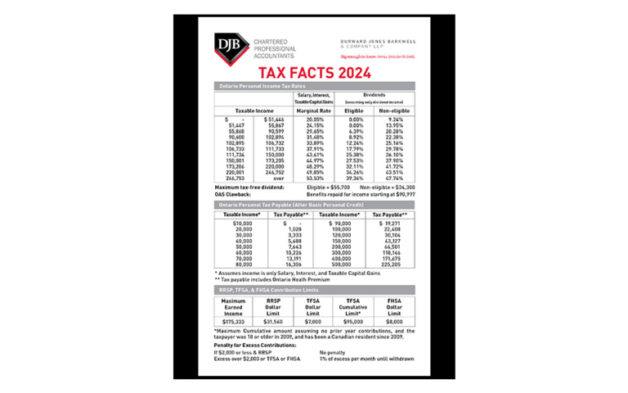

Tax Facts Card – 2024

Our History

Since 1940, Durward Jones Barkwell & Company LLP (DJB) has been providing financial and business consulting services to companies of all sizes. We can assist with complex mergers and acquisitions or guide you through the many facets of starting a small business. We do all this while remaining personally involved with our clients and the communities where we work and live.

Our professionals service clients locally, nationally, and internationally, offering industry-specific advice to clients in several industries, including agribusiness, construction & real estate, general contracting, healthcare, manufacturing & distribution, not-for-profit, professional services, tourism & hospitality, transportation, and wineries.

To learn more about our history, download the printable pdf.