Summary: Strong year-end tax planning can strengthen compliance and improve cash flow. With the end of the fiscal year approaching, private companies across Ontario and Canada have a critical window to optimize their tax position. In this article, Aprio tax leaders offer some tips to help Canadian-controlled private corporations (CCPCs) and other small and mid-sized businesses plan their tax activities for success.

Even if you treat tax planning as more than a once-a-year event, year-end planning is a crucial final step to close the fiscal year and help ensure there are no surprises with your tax liability come filing season.

As a Canadian business, it’s important to make the most of your tax position to reduce the risk of unexpected liabilities, better manage your cash flow, and make smarter strategic business decisions for the current year and the year ahead.

Here are nine ways you can practice proactive tax planning at year-end.

1. Confirm Your Corporate Tax Rate and Use the Small Business Deduction

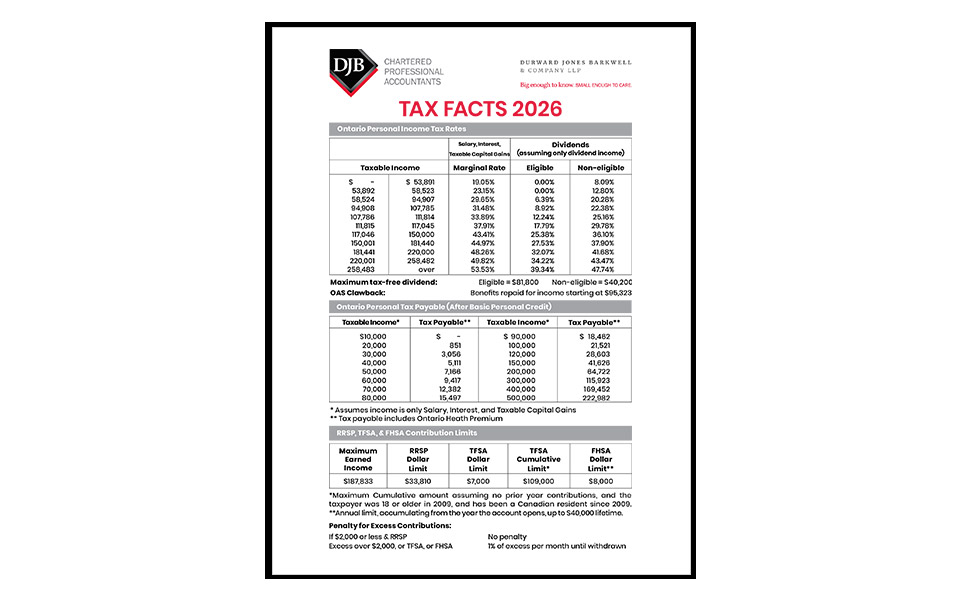

For the fiscal year ending March 2026, the Canadian federal small business tax rate remains 38% of income, or 28% after the federal tax abatement. However, for most small businesses, the tax rate will remain at 9% of the first $500,000 of active business income, where the 19% small business deduction (SBD) is applied. Zero-emission technology manufacturers may qualify for a further reduction to 4.5%.

To qualify for this rate, the company must be a Canadian-controlled private corporation (CCPC), and the income must meet that “active” status. Leveraging this deduction is the smartest tax move smaller Canadian businesses can make and should be a year-end priority.

Provinces then apply an additional small business rate, which is currently 3.2% for Ontario. Businesses must monitor two erosion factors:

- The federal deduction limit is reduced if taxable capital exceeds $10 million and is eliminated at the $50 million threshold.

- Earning more than $50,000 in passive investment may also impact it.

Reviewing these thresholds before year-end helps determine whether income should be accelerated or deferred, and whether investments should be structured differently to keep the SBD.

2. Review Capital Asset Purchases for the CRA’s Accelerated Investment Incentive

The Accelerated Investment Incentive from the Government of Canada offers an enhanced first-year depreciation allowance for specific eligible properties meeting the capital cost allowance (CCA) rules. Typically, this allows for up to 1.5x the net addition in the first year and suspends the half-year rule. If your business plans to acquire equipment, machinery, or technology, this can significantly boost your CCA deductions.

For manufacturers in Ontario specifically, capital improvements can be a major competitive driver. Be sure to review classes such as:

- Class 50 (computer equipment)

- Class 53 (manufacturing machinery with enhanced write-offs)

- Class 12 (tools and software)

Be sure to take these new rules into consideration and remember that assets must be operational and available for use in order to qualify as you plan significant purchases.

3. Evaluate Owner Compensation: Salary vs. Dividends

As a business owner, reviewing how you are compensated and understanding how that affects your tax liability is essential to year-end tax planning. The CRA offers guidance on the different tax implications for salary vs. dividends, and there’s no one correct answer. The best mix will depend on the business and the owner’s personal income needs, as well as retained earnings. However, consider these factors:

Salaries:

- Can create favourable retirement (RRSP) contribution room for the following year

- Are deductible for the corporation when paid within half a year of year-end

- Require formal payroll remittances and compliance work

Dividends:

- Are not deductible for the business

- Do not create RRSP room

- Can lower personal tax, depending on income

Many Canadian business owners use a blended approach to maximize benefits on both sides. Year-end is the ideal time to determine the most tax-efficient combination.

4. Manage Instalments and Year-End Tax Payments

If your tax liability is greater than $3,000, either this year or in the two prior tax years, you must make instalment payments, per CRA regulations, to be paid monthly or quarterly depending on eligibility.

Canadian businesses’ year-end tax planning should include:

- Reconciling what is paid to date

- Identifying any shortfall

- Making sure year-end payments are made on time

The CRA requires most corporations to pay any outstanding taxes within two to three months after year-end. Failing to meet this timeline will trigger non-deductible interest charges, which is a waste no business needs.

5. Review Income Splitting and Reasonableness Rules

The Tax on Split Income (TOSI) rule continues to apply to many private business structures. These rules restrict dividends paid to family members unless they meet very specific exclusions around their involvement, age, and ownership stake.

In Ontario specifically, many family-owned businesses use multi-shareholder structures for tax efficiency and succession planning so reviewing TOSI is essential. Confirm:

- Whether family members meet/still meet relevant criteria

- The reasonableness of salaries paid to relatives

- That all documentation of business involvement is present

TOSI compliance avoids a year-end shock when taxed punitively at the highest marginal rate for non-compliance.

6. Clean Up Shareholder Loans and Intercompany Balances

Under Canada’s Income Tax Act, shareholder loans typically must be repaid within one year of the business’s tax year. Otherwise, it will be treated as shareholder income. Year-end tax planning for Canadian businesses should always include a review of:

- Draws taken in the fiscal year

- Loans still outstanding

- Repayments needed to avoid tax consequences

Additionally, if your business is operating inter-provincially or across borders, intercompany transactions must also be properly documented and aligned with CRA guidelines.

7. Review Expense Documentation and Deductibility

Although the CRA has made moves to reduce compliance needs for smaller businesses, that doesn’t mean the documentation for small business deductions isn’t subject to intense scrutiny. Before year-end, businesses should verify their records across:

- Business-use vehicle logs

- Home-office expenses for owner-managers

- Meals and entertainment (with strict limits)

- Business travel expenses

- Digital tools, SaaS subscriptions, and technology investments

In Canada, documentation requirements are national and uniformly enforced across provinces.

8. Consider Bonuses and Year-End Accruals

Paying year-end bonuses? They can be a good strategy to reduce taxable corporate income, and may be deductible in the current year, if you pay them out within 180 days of year-end. However, the arrangement must be bona fide, and you must respect the payment timeline.

9. Plan for Upcoming Tax Changes

Good tax planning for Canadian businesses shouldn’t just be reactive. Now is a great time to proactively plan for the coming fiscal year, as well as wind down the one you are in. Businesses should take some time to review upcoming changes announced in federal or provincial budgets. For example, Budget 2024 announced federal changes to capital gains inclusion rates. November 2025 also saw Bill C-15 introduced, with significant incentives for clean technology and other notable tax position changes.

When you plan not just for this tax year but for upcoming legislative adjustments, you can significantly improve your business’s overall tax position and make sure you are prepared for the new year. Addressing your year-end tax planning in a timely fashion allows you to make informed decisions that support your financial stability and long-term growth.

Please connect with your advisor if you have any questions about this article.

This article was written by Aprio and originally appeared on 2026-01-28. Reprinted with permission from Aprio LLP. © 2026 Aprio LLP. All rights reserved. https://www.aprio.com/insights-events/top-year-end-tax-planning-tips-for-canadian-businesses-ins-article/

“Aprio” is the brand name under which Aprio, LLP, and Aprio Advisory Group, LLC (and its subsidiaries), provide professional services. LLP and Advisory (and its subsidiaries) practice as an alternative practice structure in accordance with the AICPA Code of Professional Conduct and applicable law, regulations, and professional standards. LLP is a licensed independent CPA firm that provides attest services, and Advisory and its subsidiaries provide tax and business consulting services. Advisory and its subsidiaries are not licensed CPA firms.

This publication does not, and is not intended to, provide audit, tax, accounting, financial, investment, or legal advice. Any tax advice contained in this communication (including any attachments) is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or under any state or local tax law or (ii) promoting, marketing or recommending to another party any transaction or matter addressed herein. Readers should consult a qualified tax advisor before taking any action based on the information herein.