A July 28, 2022, Tax Court of Canada case considered whether input tax credits (ITCs) in respect of a farming operation’s expenditures were available. The farming activity consisted of breeding and racing various horses and involved at least four full-time employees at one point. Over a nine-year period (2007 2015), the operations never experienced positive net earnings and more than $4 million in losses were accumulated. The owner partially financed operations with earnings from his law practice.

In order for ITCs to be available, supplies must have been made in the course of a commercial activity. For a commercial activity to have occurred, there must have been a reasonable expectation of profit.

The Court considered the following criteria when determining whether the taxpayer carried on a commercial activity:

profit and loss experience;

the taxpayer’s training;

the taxpayer’s intended course of action; and

the capability to show a profit.

Taxpayer loses

While the Court noted that the taxpayer was clearly passionate and knowledgeable about horses and had invested significant funds and time, it was insufficient to demonstrate that there was a reasonable expectation of profit. Ultimately, the Court found that the taxpayer’s lack of financial organization (he did not have financial statements) and lack of financial tools left him without the ability to diagnose the causes of his farm losses. Without the ability to understand the losses, he did not have the ability to truly stem them, and therefore he did not have a reasonable expectation of profit. The ITCs were denied.

ACTION ITEM: Ensure to sufficiently compile financial records and information such that you can reasonably identify the profitability problems in your operation.

The Canadian Income Tax law states that taxpayers are deemed to dispose of all of their property at fair market value immediately prior to death. This can result a significant income tax liability in the year of death. If the estate includes shares of a small business, the lack of funds to pay this liability may make it difficult to continue the business and keep it in the family. This deemed disposition can be deferred when assets are left to a spouse or a spousal trust, but this is only a temporary solution to the problem and does not solve the problem when the shares are transferred to the children.

The purpose of an estate freeze is to transfer the future increase in the value of assets to other individuals. In most cases, this would be other family members but could also include a key employee of the family business. The transferor retains the current value of his/her shares and defers the income taxes on the capital gain to the time of their actual or deemed disposition.

By entering into a freeze transaction, the transferor can determine the taxes that will be due on his/her death. Knowing what the future liability will be makes it easier to plan. For example, a life insurance policy may be considered as an option to fund the liability.

To accomplish the estate freeze an owner of a small business corporation exchanges his/her common shares for fixed value preference shares with dividend rights. New common shares are then issued to the new shareholders. They will enjoy the benefits of the future growth of the business. This will result in a lower capital gain on the deemed disposition when the transferor dies. One of the reasons for a freeze is to transfer the business to the next generation. However, consideration must be given to the share structure to allow the transferor to retain control of the business and, if he/she wants, provide a source of income by paying dividends on his/her freeze shares.

Careful consideration must be given to the value of the shares of the corporation that is being frozen. In many cases, it is recommended that a Chartered Business Valuator be engaged to determine the value of the shares. Unwanted tax consequences could result if the Canada Revenue Agency successfully challenges that the value of the fixed value preference shares does not line up with the value of the corporation at the time of the freeze.

What should be done if you as the business owner want to enter into an estate freeze but you are not sure whom you want the future growth to go to or your children are too young to have share ownership? In this situation, it would be a great idea to create a family trust to hold the new common shares. A family trust allows you to put off this decision for up to twenty-one years. Beneficiaries of the trust normally include all family members. At some date in the future, the trustees of the trust give the shares to the chosen beneficiaries. This is a non-taxable event. To provide for maximum flexibility, the business owner would also be a beneficiary of the trust in the event he/she decides not to transfer future growth and effectively decides to cancel the freeze. In certain circumstances income splitting can be achieved by paying dividends to the trust and then allocating the funds to beneficiaries. It is recommended that you seek professional advice before undertaking such tax planning and to help with the creation of a family trust.

Often the freeze shares that the transferor receives are redeemed over a number of years as part of their retirement income. This spreads out the tax liability and reduces the liability to their estate.

Individuals who have a significant portfolio of investments may want to consider implementing an estate freeze. To do so they would incorporate a holding company in which to transfer the portfolio. At the end of the transactions, the individual will own fixed value preference shares of the holding company and possibly a note receivable from the holding company with a combined value equal to the value of the stock portfolio. Other family members or a family trust will hold the common shares. Careful planning is required, including proper tax filings in order to transfer the portfolio to the holding company on a tax-deferred basis. In addition, the transferor needs to be aware of and to plan around the corporate attribution rules of the Income Tax Act, which could have a negative effect on the planning for years into the future.

In summary, an estate freeze can be a very good tax-planning tool but there are a number of items that must be addressed and considered before undertaking such a plan. A bad plan could result in an unwanted tax bill. The plan should be tailored to fit your needs.

The post-pandemic evolution of office and multifamily

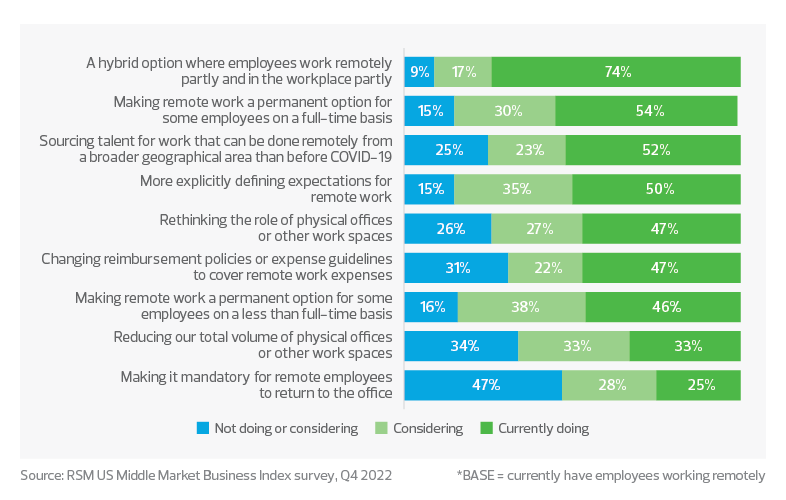

Throughout the pandemic, a familiar storyline emerged: Traditional office workers found themselves suddenly mobile, empowered by a fully remote work phenomenon brought on by the COVID-19 pandemic. The term “workcation” became mainstream as many chose to work remotely from the Sun Belt and other attractive locations popularized during the time of social distancing and lockdowns. While some corporations, including Goldman Sachs, Walmart, Bank of America, and Tesla, have called their workers back to the office, most—including tech giants Google, Amazon, and Microsoft—have staunchly affirmed their commitment to new hybrid protocols.

In fact, nearly three-quarters (74%) of middle market companies have rolled out a hybrid work option for employees, according to responses to workforce questions in RSM’s Middle Market Business Index survey for the fourth quarter. And only one-fourth said their organizations were requiring workers to return to the office.

It’s increasingly clear that the norms of work and residential life are being redefined in real time for real estate owners and operators.

Based on experience with people working remotely, which of the following is your organization currently doing or considering?*

Office reform hinges on flexibility

In the office realm, the primary challenge is meeting the expectations of all stakeholders—investors, business leaders, and employees. Surveys abound highlighting a disconnect in sentiment between employees and business leaders in the execution of the hybrid work model of the future, with leaders preferring an office-centric model and staff favoring being predominantly remote; however, the data also indicates that employees and business leaders alike are now prioritizing flexibility, collaboration, and digital investment.

Office investors have a unique opportunity to capitalize on this alignment by building the foundation of the office of the future, designing and retrofitting spaces to make use of flexible space, offering appealing open layouts that foster teamwork, deploying technology that allows both in-person and digital collaboration, and allowing tenants shorter-term leases based on usage or a revenue-sharing management agreement.

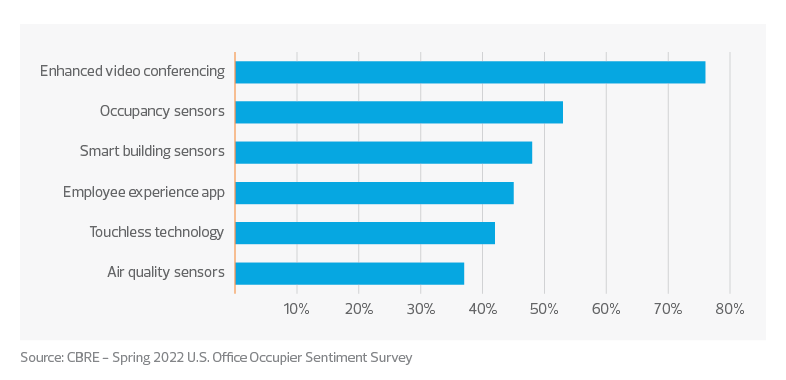

Which of the following commercial real estate technologies are you using or considering for the future steady state?

Flexible, home-centric future emerges in residential space

Adam Neumann, founder of coworking space WeWork, is placing another bet on flexible space—this time in the residential market. “Flow,” Neumann’s newest venture, is slated to bring experiential, purpose-built living to the residential market by offering furnished residences, flexible leases, and the promise of vibrant, connected communities. Set to launch next year, Flow is counting on the fact that the nomadic, work-from-anywhere trend unleashed by the pandemic is more than a passing fad. Its target population is younger workers, often in tech jobs, who split their time among several cities but still crave a sense of community. Neumann has amassed critical backing from anchor investor Andreessen Horowitz, which made a $350 million investment, reportedly valuing Flow at over $1 billion, according to The Real Deal.

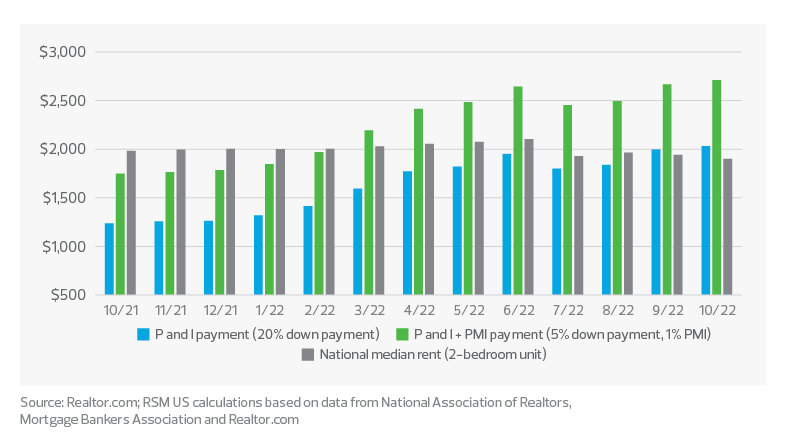

The flexible community isn’t the only strategy gaining momentum with investors; single-family rentals are increasingly popular as higher median home prices and rising mortgage rates, which hovered around 7% in November, now make purchasing a house more expensive than renting in markets across the United States.

Recent capital flows continue to chase opportunities in the single-family rental market, according to Yardi Matrix, which noted that through August 2022, institutional investors had committed more than $60 billion to buy single-family homes; Yardi pegged the growth on the build-to-rent market. Besides higher home prices, the rental trend is being fueled by the decline in new construction and housing starts and higher construction costs.

However, increasing interest in this space by institutional investors has met with resistance from federal policymakers. A meeting of the Oversight and Investigations subcommittee of the U.S. House Committee on Financial Services in late July focused on how expanding ownership of single-family rentals by institutional investors is putting affordable housing further out of reach for first-time homebuyers. Washington may indeed have cause for concern when it comes to future housing affordability: Research conducted this summer by MetLife Investment Management forecasts that by 2030, institutions will own more than 40% of all single-family rentals, eight times the estimated current 5% of the 14 million single-family rentals.

Monthly rent vs. monthly payment, median-priced home, 30-year mortgage

Technology is top priority for investors

Investment in technology has become critical not only for the future of commercial offices but also for multifamily and single-family rentals. Players in the residential rental space are focused on incorporating tech solutions to drive resident engagement, develop robust rental pipelines, manage revenue, and increase operational efficiencies. Priority investments include those that offer digital experiences for residents (keyless entry, environmental controls, communication with management, etc.) and that aggregate property-level data to enable proactive asset management through data analytics.

Market-leading public REITs point to investment in innovative technologies for margin improvement and future growth. Meanwhile, the proliferation of disparate smart home technologies has yielded platforms that unify Internet of Things (IoT) devices. One example is SmartRent, which enables multi- and single-family operators to manage remote access to smart devices throughout the tenancy life cycle: resident move in/move out, access to units for self-guided showings, routine maintenance and more. SmartRent and other solutions to manage remote access are a game changer for operators, allowing for reduced staffing that trims overhead and provides enhanced data analytics.

Market participants are looking to differentiate their properties with best-in-class technologies. They are gaining a front seat to emerging solutions through venture capital arms or partnerships with technology incubators, recognizing the importance of digital transformation to their ongoing success.

RSM Canada Alliance provides its members with access to resources of RSM Canada Operations ULC, RSM Canada LLP and certain of their affiliates (“RSM Canada”). RSM Canada Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each are separate and independent from RSM Canada. RSM Canada LLP is the Canadian member firm of RSM International, a global network of independent audit, tax and consulting firms. Members of RSM Canada Alliance have access to RSM International resources through RSM Canada but are not member firms of RSM International. Visit rsmcanada.com/aboutus for more information regarding RSM Canada and RSM International. The RSM trademark is used under license by RSM Canada. RSM Canada Alliance products and services are proprietary to RSM Canada.

DJB is a proud member of RSM Canada Alliance, a premier affiliation of independent accounting and consulting firms across North America. RSM Canada Alliance provides our firm with access to resources of RSM, the leading provider of audit, tax and consulting services focused on the middle market. RSM Canada LLP is a licensed CPA firm and the Canadian member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM Canada Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise, and technical resources.

For more information on how DJB can assist you, please contact us.

“Working capital” is the capital of a business which is used to fund day-to-day operations and meet shortterm obligations. In its most basic form, working capital is calculated as a business’ current assets, less its current liabilities.

However, in open market transactions and notional business valuations certain current assets and liabilities are often excluded when assessing the “operating” or net trade working capital of a business, such as cash, shareholder/related party loans, and other non-operational amounts. Cash is generally excluded from net trade working capital of privately held businesses unless the cash is used directly in the operations of the business, such as cash kept in cash registers in a retail business. This is because in most cases, the cash held in a business accumulates as a result of operations (i.e., through net income earned), and that cash is available to be either reinvested in the business or to be withdrawn by the owners, and is therefore not necessary in order to maintain the existing operations. In simple terms, net trade working capital is related to the operating activities of a business (excluding cash) such as accounts receivable, inventory, prepaid expenses, accounts payables, and accrued liabilities.

Calculating Working Capital

Determining which line items should be included in working capital may involve some judgment and is not always simple because the makeup of working capital can vary widely across different industries and even from business to business. This is why it is important to consider the specific nature of the operations of a business that impact how it employs working capital, as well as broader working capital issues that are common in the industry. Additionally, each component of working capital may need to be examined further to ensure all balances within the account are up-to-date, are operational and belong in working capital, and that the value reflected in the financial statements does not over or under-represent the asset or liability. Finally, the accounting standards used in the source financial statements should also be considered when calculating working capital, as balances on the balance sheet may be calculated differently depending on the accounting standards applied (i.e., GAAP, ASPE, IFRS).

Normalized Working Capital

In cases when the value of a business is determined based on its ability to generate future cash flows (i.e., using an income/earnings based methodology as opposed to an asset based methodology), the working capital that is required to operate the business is included in this value, and is not added to the value of the business. This is because the businesses requires the working capital to fund its continued operations and generate the level of income that this value is based. The amount of net trade working capital required to maintain ongoing operations is commonly referred to as the “normalized” net trade working capital amount.

Working Capital in a Business Sale

When a business is sold, it is common for the letter of intent between the buyer and seller to include general terms stating that the business will be sold with a sufficient level of working capital for the new owner to maintain operations. As the transaction advances, a specific amount of “target working capital” is usually agreed upon by both parties with corresponding definition on how the target working capital is to be calculated. This represents the amount that the buyer and seller agree is required to maintain operations, and that is expected to be left in the business at the time of closing. This target amount is based on an analysis of the company’s historical financial results, industry norms, ratio analysis, and benchmarks, and is ultimately determined through negotiations between the buyer and seller.

Working capital in a business at any one point in time is not always representative of the ongoing amount required. In some businesses and industries, the working capital required changes dramatically due to timing, such as large projects completed and invoiced, from month to month or year to year, such as businesses that experience seasonality or are in cyclical industries. For these types of businesses, it may be necessary to examine the average working capital requirement across different periods. Working capital balances may also be higher or lower than the required amount simply due to management’s own preferences. For these reasons, it is important to determine working capital requirements for a business on a normalized basis, which includes adjustments for seasonality or irregular changes that are not related to normal operations.

Implications on Price

When the amount of working capital left in the business on the day the sale of the business closes is different from the previously agreed upon target working capital amount, there is usually an adjustment made to the sale price to reflect this difference. In transactions where the actual working capital is less than the target, this negatively impacts the seller because the sale price is usually reduced by this amount. When the actual working capital is greater than the target, an increase to the sale price may be warranted. In a notional valuation context, a similar adjustment should also be considered if the working capital of the subject business is higher than or below what would be considered “normal” on the valuation date with a corresponding adjustment to the valuation conclusion of the shares.

The process for negotiating working capital in a business sale usually follows these broad steps:

A letter of intent is developed, outlining the broad terms agreed to by the buyer and seller. This usually includes an agreement that there will be a “normal” level of working capital in the business.

The buyer will analyze financial information about the business, which is supplied to them in order to better understand the working capital requirement of the business.

During the due diligence phase, both parties continue to analyze information about the business to determine any potential adjustments to working capital.

Through negotiations , b o t h parties will eventually come to an agreement on the “target working capital”.

A purchase agreement is drafted, and will further define how working capital is calculated and the target amount agreed to.

The purchase agreement is finalized, and additional clauses may be added outlining a post-closing dispute resolution process (including working capital disputes).

Post-closing , the buyer will determine the actual working capital level that was in the business at close and further discussions may take place between the buyer and seller to determine any post-closing adjustments.

If necessary, the dispute resolution process is initiated as outlined in the purchase agreement to remedy any disputes between the buyer and seller.

At DJB, our team of specialists have the professional experience to assist business owners and prospective buyers throughout the transaction process. Our trusted professionals can assist in many aspects of business sales and purchases, including assessing the complex issues involved in determining the value of a business and analyzing its working capital requirements.

The information contained herein is general in nature and based on authorities that are subject to change. RSM Canada guarantees neither the accuracy nor completeness of any information and is not responsible for any errors or omissions, or for results obtained by others as a result of reliance upon such information. RSM Canada assumes no obligation to inform the reader of any changes in tax laws or other factors that could affect information contained herein. This publication does not, and is not intended to, provide legal, tax or accounting advice, and readers should consult their tax advisors concerning the application of tax laws to their particular situations. This analysis is not tax advice and is not intended or written to be used, and cannot be used, for purposes of avoiding tax penalties that may be imposed on any taxpayer.

RSM Canada Alliance provides its members with access to resources of RSM Canada Operations ULC, RSM Canada LLP and certain of their affiliates (“RSM Canada”). RSM Canada Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each are separate and independent from RSM Canada. RSM Canada LLP is the Canadian member firm of RSM International, a global network of independent audit, tax and consulting firms. Members of RSM Canada Alliance have access to RSM International resources through RSM Canada but are not member firms of RSM International. Visit rsmcanada.com/aboutus for more information regarding RSM Canada and RSM International. The RSM trademark is used under license by RSM Canada. RSM Canada Alliance products and services are proprietary to RSM Canada.

DJB is a proud member of RSM Canada Alliance, a premier affiliation of independent accounting and consulting firms across North America. RSM Canada Alliance provides our firm with access to resources of RSM, the leading provider of audit, tax and consulting services focused on the middle market. RSM Canada LLP is a licensed CPA firm and the Canadian member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM Canada Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise, and technical resources.

For more information on how DJB can assist you, please contact us.

On Aug. 9, 2022, the Canadian Department of Finance released draft legislation containing proposed targeted amendments to the foreign accrual property income (FAPI) rules to prevent taxpayers from gaining a tax deferral advantage by earning certain types of income (including investment income) through controlled foreign affiliates (CFAs) that are held by Canadian-controlled private corporations (CCPCs) and substantive CCPCs (SCCPCs). These proposed amendments apply to taxation years ending on or after April 7, 2022.

Background

Certain passive income (including investment income) earned by a CFA of a Canadian taxpayer is included in the Canadian taxpayer’s income on an accrual basis as FAPI. If the Canadian taxpayer is a CCPC, it is potentially not liable to tax on the FAPI because of the offset available due to the current relevant tax factor (RTF) of four. That is, if the CFA pays a foreign tax of at least 25 per cent, the CCPC can claim a foreign accrual tax (FAT) deduction of four times the FAT which results in a complete deferral of Canadian tax on FAPI earned by a CCPC until amounts are paid out to individual shareholders as dividends. However, a similar income earned by the CCPC in Canada would have been subject to a tax rate of approximately 50 per cent, which is why the government introduced the change.

The most recent budget and the draft legislation proposed to amend the RTF for CCPCs and SCCPCs to 1.9 such that there will be some income inclusion for CCPCs and SCCPCs from FAPI earned by their CFAs. This will result in immediate tax implications on the CCPCs and the SCCPCs as illustrated below.

For illustration purposes, assume a CFA earns a FAPI of $1,000 and pays a foreign tax of 25 per cent (i.e., FAT of $250) and no withholding tax is applicable. The below considers the tax implications on the payment of dividends by the CFA to its Canadian parent corporation (Canco).

Description

Current rules

Proposed rules

Notes

Income earned by the CFA

$1,000

$1,000

Income tax paid by the CFA

$(250)

$(250)

25% of income earned by the CFA

Cash remaining with the CFA

$750

$750

FAPI

$1,000

$1,000

FAT deduction

$(1,000)

$(475)

RTF foreign tax*

Net FAPI

$-

$525

Canco’s Canadian corporate tax

$-

$264

50.2% of CCPC’s investment income

The refundable portion of Canadian corporate tax

$-

$161

30.67% of CCPC’s investment income

The permanent portion of Canadian corporate tax

$-

$103

*The current RTF is four. The government has proposed to change the RTF to 1.9.

Further, to address integration as a result of the changes to the RTF, certain amendments have been proposed to the capital dividend account (CDA), the general rate income pool (GRIP), and the low rate income pool (LRIP). Although there are proposed amendments to LRIP, for the purposes of this article, we will focus on the CDA and the GRIP account.

CDA allows amounts that have borne a sufficient level of tax to be declared tax-free to the shareholders. Although the calculation for CDA is long and complex, the most common inclusion is the non-taxable portion of capital gains. The draft legislation has proposed to add to the CDA the amount computed as (RTF-1) multiplied by foreign income tax paid by the CFA less any withholding tax paid in respect of the dividend (our illustration did not consider a withholding tax in the foreign jurisdiction). From the example above, $250 multiplied by (1.9-1), or $225, would be added to the CDA of the Canadian recipient corporation which can be paid tax-free to its shareholders.

GRIP reflects the amount of a corporation’s after-tax income that was subject to tax at the general corporate tax rate. The existing legislation adds to the GRIP all amounts that are received as dividends from FAs to the extent they are deductible under section 113 of the ITA. The draft legislation proposes to remove from GRIP of a CCPC the amounts that would be deductible under section 113 (applies to amounts paid from hybrid surplus or taxable surplus). However, amounts paid from exempt surplus (or pre-acquisition surplus) can still be added to the GRIP.

From the example above, under the existing legislation the entire amount of dividends received from the CFA, i.e., $750, are added to the GRIP which can be paid as eligible dividends to Canco’s shareholders. However, subsequent to the passing of the draft legislation, no amount would be added to the GRIP. Instead, the amount of taxable dividend would be declared as a non-eligible dividend which is subject to a higher tax.

The below table illustrates the tax implications when Canco receives the dividends from its CFA and pays them to the shareholder. Please assume no withholding tax for the purposes of the illustration.

Description

Current rules

Proposed rules

Notes

Dividends paid by CFA to Canco

$750

$750

Cash remaining with the CFA (from the table above)

Deduction in respect of dividend from FA

$(750)

$(225)

Under para 113(1)(b) of the ITA*

Deduction under subsection 91(5)

$-

$(525)

Deduction is available to Canco to avoid double taxation on FAPI that was already included in its income on an accrual basis (refer to table above)

The amount available to distribute to shareholder

$750

$647

**

The portion of the dividend that can be declared as a capital dividend

$-

$225

***

The portion of the dividend that can be declared as an eligible dividend

$750

$-

****

The portion of the dividend that can be declared as a non-eligible dividend

$422

*****

Personal tax on eligible dividend

$295

Assuming the highest tax rate of 39.34% in Ontario

Personal tax on non-eligible dividend

$201

Assuming the highest tax rate of 47.74% in Ontario

*Tax deduction computed as (RTF-1) * foreign tax paid.

**Computed as FAPI less permanent portion of corporate tax from the table above.

***Under the proposed rules, the amount computed as (RTF-1)* foreign tax paid is added to the CDA pool that can be declared tax-free to shareholders.

****Under the current rules, this amount of deduction under subsection 113(1), see * above, is added to the GRIP and can be declared as an eligible dividend.

*****Under the proposed rules, only non-eligible dividends can be declared on investment income.

The effective total tax rate

Current rules

Proposed rules

Income tax paid by the CFA

$250

$250

CCPC corporate tax (permanent portion)

$-

$103

Personal tax on eligible dividends (immediate)

$-

$-

Personal tax on non-eligible dividends (immediate)

$-

$201

Personal tax on eligible dividends (deferred)

$295

$-

Total personal and corporate tax

$545

$554

Total tax-deferred

$295

$-

As the illustrations above highlight, there is currently a tax deferral of $295 available to the extent Canco does not declare dividends to its shareholders immediately. This deferral will not be available once the proposed legislation is enacted.

What to do?

Shareholders of CCPCs that earn FAPI should examine their structure to understand the impact of the proposed legislation and whether there are restructuring options available to minimize the potential tax exposure.

The information contained herein is general in nature and based on authorities that are subject to change. RSM Canada guarantees neither the accuracy nor completeness of any information and is not responsible for any errors or omissions, or for results obtained by others as a result of reliance upon such information. RSM Canada assumes no obligation to inform the reader of any changes in tax laws or other factors that could affect information contained herein. This publication does not, and is not intended to, provide legal, tax or accounting advice, and readers should consult their tax advisors concerning the application of tax laws to their particular situations. This analysis is not tax advice and is not intended or written to be used, and cannot be used, for purposes of avoiding tax penalties that may be imposed on any taxpayer.

RSM Canada Alliance provides its members with access to resources of RSM Canada Operations ULC, RSM Canada LLP and certain of their affiliates (“RSM Canada”). RSM Canada Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each are separate and independent from RSM Canada. RSM Canada LLP is the Canadian member firm of RSM International, a global network of independent audit, tax and consulting firms. Members of RSM Canada Alliance have access to RSM International resources through RSM Canada but are not member firms of RSM International. Visit rsmcanada.com/aboutus for more information regarding RSM Canada and RSM International. The RSM trademark is used under license by RSM Canada. RSM Canada Alliance products and services are proprietary to RSM Canada.

DJB is a proud member of RSM Canada Alliance, a premier affiliation of independent accounting and consulting firms across North America. RSM Canada Alliance provides our firm with access to resources of RSM, the leading provider of audit, tax and consulting services focused on the middle market. RSM Canada LLP is a licensed CPA firm and the Canadian member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM Canada Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise, and technical resources.

For more information on how DJB can assist you, please contact us.

Canadian businesses continue to extend their reach into the U.S. for numerous reasons; some of which include proximity, lower corporate tax rates as a result of the 2017 US tax reform, a stable economy, and a skilled workforce. While these are all great reasons to expand operations into the U.S., companies must consider the U.S. Federal and State tax implications of carrying on a trade or business in the U.S. Note that this article does not cover U.S. state tax issues Canadian businesses may face – please contact us for further guidance on navigating such situations.

What does it mean to “carry on a trade or business in the U.S.”?

Generally, a trade or business is any activity conducted for the purpose of generating income. The threshold for this determination is fairly low in that a Canadian company could be considered to be carrying on a trade or business in the U.S. when it has considerable, regular, and continuous dealings with U.S. customers.

Effectively Connected Income and U.S. Permanent Establishments

Generally, when a Canadian company engages in a U.S. trade or business, all income associated with that trade or business is considered to be Effectively Connected Income (ECI). Note that U.S. source income may still be considered to be ECI even when there is no connection between the income and the U.S. trade or business.

Canadian companies are required to pay U.S. federal income tax on ECI (less expenses incurred to generate ECI) however, companies may seek relief from this tax burden pursuant to the U.S. – Canada income tax convention. Under the tax treaty, Canadian companies are only required to pay U.S. federal income tax if they carry on business through a U.S. permanent establishment.

Generally, a permanent establishment (PE) is defined as a fixed place of business in the U.S. through which a non-resident entity (i.e. a Canadian company) carries on business. This definition continues to evolve given the rise in e-commerce activities. Some traditional examples of a PE include:

A fixed place of business such as a branch, an office, factory, workshop, etc.

Agents who habitually exercise the authority to conclude binding contracts in the U.S. on behalf of the Canadian company.

The provision of services that meet certain specified criteria.

Pursuant to the tax treaty, the following activities generally do not give rise to a U.S. PE:

The use of facilities for storage, display or delivery of goods.

The maintenance of a stock of goods for storage, display, and or delivery.

The purchase of goods in the U.S.

Advertisement, supply of information or scientific research done in the U.S. that is preparatory or secondary to the business.

U.S. Federal Income Tax Filing Requirements

Canadian companies with income effectively connected to a U.S. trade or business must file U.S. federal income tax returns. A Canadian business with U.S. ECI that is not attributable to a U.S. PE must file U.S. Federal Form 1120-F US Income Tax Return of a Foreign Corporation and Form 8833 Treaty-Based Return Position Disclosure Under Section 6114 or 7701(b) to claim relief from U.S. federal tax pursuant to the U.S.- Canada income tax treaty. Generally, this return must be filed 5 ½ months after the taxpayer’s year-end. For example, a calendar year taxpayer must file the protective return by June 15th.

Canadian companies with U.S. ECI attributable to a U.S. PE cannot claim the treaty exemption and must file Form 1120-F to report U.S. source income and expenses. The taxpayer may claim foreign tax credits on its Canadian income tax return for any U.S. income tax paid. Generally, this return must be filed 3 ½ months after the taxpayer’s year-end. For example, a calendar year taxpayer must file the return by April 15th.

Penalties

If a return is filed late but no tax is payable due to the treaty exemption, interest and penalties may not apply if the return is filed by the second deadline which is 18 months from the original due date. If the return is not filed by the second deadline, the Canadian company may be taxed on its U.S. source gross business income. If a treaty exemption is claimed to eliminate the tax liability, a non-disclosure penalty of $10,000 may be levied for each item of income.

If a return is filed late and there is tax due, interest and penalties will be calculated based on the tax due and exposure can be quite significant

Summary

Canadian companies with activities in the U.S. may have federal income tax filing obligations and in some cases, a federal tax liability when business is conducted through a permanent establishment. Note that U.S. state income tax obligations may also apply based on the different laws of each state.

If you determine your business may have a U.S. income tax filing obligation or are thinking about expanding to the U.S., we can help. Our cross-border taxation advisors have the knowledge and expertise to help you evaluate and determine the implications for your business.

Directors can be personally liable for payroll source deductions (CPP, EI, and income tax withholdings) and GST/HST unless they exercise due diligence to prevent the corporation from failing to remit these amounts on a timely basis.

An August 31, 2022, Tax Court of Canada case found that the director was not duly diligent and therefore was personally liable for the corporation’s unremitted payroll deductions, interest, and penalties of $78,121 from January 2011 to April 2012.

The taxpayer argued that he was duly diligent as he asked at the directors’ meeting each month whether the tax remittances were up-to-date and received oral confirmations that they were. The taxpayer stated that he had “checked the box” at each directors’ meeting. He also argued that his decisions were driven by materiality; he focused his efforts on the corporation’s overall well-being and safeguarding the millions of dollars of investment, rather than the payroll remittances that he considered “tiny.”

Taxpayer loses

The Court ruled that the taxpayer was not duly diligent in preventing the failure to make adequate payments. It noted that the taxpayer never contacted CRA to confirm whether payroll remittances were current, which was particularly problematic as he was unable to obtain reliable financial statements and was aware ofthe difficult financial situation. While it was the taxpayer’s view that this was someone else’s job, there was no evidence of the taxpayer ever asking anyone else to follow up with CRA.

ACTION ITEM: Prior to accepting any role as a director, ensure to fully understand your responsibilities and potential exposure to personal liability. If currently acting as a director, make sure to be duly diligent in ensuring payroll and GST/HST payments are properly made.

Nonprofit organizations are either striving to make a bigger impact, or they are falling behind. The following infographic highlights four strategies nonprofits can adopt to help them fulfill their missions to the best of their abilities.

RSM Canada Alliance provides its members with access to resources of RSM Canada Operations ULC, RSM Canada LLP and certain of their affiliates (“RSM Canada”). RSM Canada Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each are separate and independent from RSM Canada. RSM Canada LLP is the Canadian member firm of RSM International, a global network of independent audit, tax and consulting firms. Members of RSM Canada Alliance have access to RSM International resources through RSM Canada but are not member firms of RSM International. Visit rsmcanada.com/aboutus for more information regarding RSM Canada and RSM International. The RSM trademark is used under license by RSM Canada. RSM Canada Alliance products and services are proprietary to RSM Canada.

DJB is a proud member of RSM Canada Alliance, a premier affiliation of independent accounting and consulting firms across North America. RSM Canada Alliance provides our firm with access to resources of RSM, the leading provider of audit, tax and consulting services focused on the middle market. RSM Canada LLP is a licensed CPA firm and the Canadian member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM Canada Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise, and technical resources.

For more information on how DJB can assist you, please contact us.

Among the approaches or methodologies employed by business valuators to determine the value of a business or equity interest is the market approach. The market approach determines the value of a business or equity interest using one or more methodologies that compare the subject business to similar assets, businesses, business ownership interests, and securities that have been sold or publicly traded. The advantages of using the market approach eliminates some subjective estimates and uses data that is readily available and verifiable. Two commonly applied methods under the market approach are the guideline public company method and the precedent transaction method. In this article, we will focus on the guideline public company method.

The guideline public company methodology is a useful tool in determining the value of a business or equity interest by comparing the subject company to similar companies that are publicly traded. This allows a private business to better understand the price it might receive if it was to trade publicly, based on public companies within a similar industry and similarly sized operations.

There are three steps to prepare a guideline public company comparison:

Identifying a list of comparable publicly traded companies and calculating applicable valuation multiples. A valuation multiple is applied to a financial measure such as normalized earnings before interest, taxes, depreciation, and amortization (EBITDA) to develop the value of a business;

Adjusting the guideline public company multiples based on the relative size and risk of the comparable public companies in relation to the subject company; and

Applying the selected multiples, after any adjustments, to the subject company/interest in order to determine its value.

Identifying comparable public companies and calculating valuation multiples

When identifying comparable public companies, it is important to consider the industry, operation size, location, risk, and diversity of revenue streams of the subject company. For each variable, consider the impact of relevant differences between the selected public comparable companies and the subject company. For example, classifying a restaurant into a full-service restaurant industry versus the fast-food limited service industry could result in different market multiples. Similarly, diversified companies are expected to have different market multiples compared to companies that engage in a specific line of business.

A common misconception is selecting more public companies, will result in a better analysis when the public companies may not be truly comparable to the subject company. Ideally, an average of a number or group of comparable public companies should be used for an accurate analysis.

Once a set of public comparable companies have been identified, valuation multiples are calculated using either the Enterprise Value or Equity Value. Both can be applied to earnings before interest and taxes (EBIT), EBITDA, revenue, or even nonfinancial measures. When calculating the valuation multiples, review the public company’s financial reports for one-time adjustments that may affect EBITDA or the selected measure. The most common valuation multiples use the Enterprise Value, being the “debtfree” approach. The Equity Value may be more relevant and reliable for equity valuations. See our Spring/ Summer 2022 issue of the FSAT News for an in-depth discussion on the differences between Enterprise Value and Equity Value.

Adjusting guideline public company multiples for comparability to private companies

Professional judgment is required to determine the potential discounts that is applicable to the subject company. For example, an inherent minority discount applicable to public traded companies may offset a liquidity discount that is applicable to smaller private companies. The following are common discounts to public company valuation multiples when valuing smaller private companies:

Liquidity discount: The amount by which the en bloc value of a business or ratable value of an interest therein is reduced in recognition of the expectation that the business or equity interest cannot be readily converted to cash.

Minority discount: The reduction from the pro rata portion of the en bloc value of the assets or ownership interests of a business as a whole to reflect the disadvantages of owning a minority shareholding.

Size discount: Large, diversified, and attractive businesses may have little or no discount, whereas smaller companies may have considerable discounts.

Applying selected valuation multiples

Finally, prior to applying the selected Enterprise or Equity Value multiples to the subject company, ensure the earnings of the subject company are “normalized” so they are representative of future maintainable earnings and are similar to the earning measure of the comparable public companies.

The market approach is often used as a secondary methodology or to assess the reasonability of a valuation conclusion. However, it can also be an informative first step if you are considering selling your business or adding a shareholder. To ensure you consider accurate guideline public comparable companies multiples for your business, one of our valuation specialists may be able to assist.